Sometimes it’s better to get in early on a company, even if it means the stock will fall in price early on… than getting in after a stock’s meteoric rise, risking you being left holding the bag. Today we look at one company that could go either way, Snowflake, arguably one of my riskiest holdings from a valuation perspective, but no-brainer in terms of market opportunity.

Snowflake: Visionary or Bagholder?

Snowflake reported earnings yesterday. I first wrote about Snowflake in Jan 2021. I considered shorting the stock when it hit $429/share in early January, as it briefly commanded a market cap greater that than of IBM (at $110 billion). Shorting means selling a stock you don’t own at a given price on the assumption that you can buy it at a lower price, locking in a retroactive profit. It’s very risky, because if the share price goes up, your losses are technically unlimited. When I published my piece, the stock had fallen to $268/share but was still pricey by any traditional, reasonable metric.

Atlassian and Twilio, two broad comparables, were valued at some $50 billion then. If investors search for growth, Twilio’s market value looks suspect based on the slowing growth (30%) in the face of a massive spike in market value in the past year. There’s no doubt that Snowflake is growing quickly, and much faster: growing quarterly revenue from $28.7 million to $190.5 million in nine quarters is impressive!

Moreover, Snowflake may have benefited from the halo effect of bragging about Warren Buffett scooping up some shares, but as the sage of Omaha bought stock pre-IPO at a relatively low[er] price, that didn’t really weigh in my analysis. Indeed:

The company said that the midpoint of its pricing range for the IPO is expected to be $80 per share, which would value Berkshire Hathaway’s stake at more than $550 million at the time it goes public. At that price, Snowflake would have a market cap of $22.3 billion, based on the latest shares outstanding count in the prospectus, marking an almost $10 billion increase since February, when Salesforce led a financing round at a $12.4 billion valuation.

Now granted, Covid has accelerated trends and executives and companies who were dragging their feet before embracing the cloud have now found religion and doing so with greater fervor.

Nonetheless, Snowflake benefited from hype and irrational exuberance: that $429/share gave it a valuation that was six times its’ original, targeted IPO price. Today the market value is twice the IPO price, which is actually not crazy given IPO shares are priced to pop, but still, Snowflake seemed like a modern day Icarus, flying too close to the sun, and thus melting away, especially with the subsequent March lockup period. However, considering Tesla’s jaw-dropping, gravity-defying rise and that short-sellers lost $50 billion in 2020 alone, I didn’t short it despite the nosebleed $120 billion market cap.

I knew the price would fall, but given my long term horizon, I began to research the company to find out what the hype was all about.

Data is the New Oil

Snowflake’s offering is compelling: companies are using more and more cloud-based services and software, having a global data warehousing solution and central dashboard to manage them all is indeed a valuable service. The company total addressable market opportunity is approximately $81 billion.

The bigger tech companies have similar products, like Google Cloud’s BigQuery, Amazon AWS’ Redshift, Microsoft Cosmos. But Snowflake’s solution can be used in conjunction with any cloud service, whereas others cloud computing services and data management software tend to be inseparable. Businesses could not mix and match between products, and tools from one provider couldn’t be used with data stored elsewhere.

Not all companies have the same revenue upside, some companies charge flat fees for access to their software and services, Snowflake brags about usage-based pricing. With data usage exploding, that is definitely the preferred model.

Can Snowflake be the next Salesforce?

To me, the company I thought of was less IBM, Twilio or Atlassian, but Salesforce, which provides customer relationship management (CRM) service and a complementary suite of enterprise applications focused on customer service, marketing automation, analytics, and application development.

Salesforce and Snowflake are existing technology partners, and Salesforce invested $250 million along Berkshire Hathaway’s investment. But their current, actual holding may be less. Investing because someone else did so is literally the definition of the greater fool theory.

Demand for Data is Much Larger Than Demand for CRM

Nonetheless, as a CEO of a digital media who’s seen demand for data soar, it’s not unthinkable to envision a future where the company that commands an enviable position in data warehousing would command a massive valuation. While the company’s competitors are a who’s who in technology, that also creates an opportunity for Snowflake to become an acquisition target or merger candidate over time.

As the stock tumbled into the $200s, I knew it remained wildly expensive by any fundamental analysis, but I decided to go long and bought some shares based on my very long term horizon in my more “aggressive” growth-oriented fund, which consists of three buckets:

a) bets on fairly speculative tech and digital media companies that probably don’t meet a more conservative investment criteria but at market capitalizations of under $50 billion can grow into $100 billion – $500 billion dollar businesses thanks to their leadership in markets and the boundaryless, global nature of the Web;

b) larger (relative to the professionally managed fund) long-term investments in “blue chip tech firms” like Google, Amazon, Apple, etc.

c) bets in IPOs that may be volatile in near term but in 5-10 years could go to $0 or be worth 10X.

Analysts are all over the place: some remain bullish, others bearish. The distinction seems to boil down to time horizon. The reality is demand for data is infinitely larger than demand for CRM tools.

Snowflake, which was founded in 2012, hit $1 billion in revenues nine years after being founded. But Snowflake’s valuation post-IPO made no sense ($1 billion in revenues commanding $110 billion in market cap, the same as IBM!) but now that the stock has fallen by half, that $300 average 1-year target for the stock price makes it slightly more enticing in the mid-term, which then makes its long term potential somewhat more attractive.

Salesforce was founded in 1999, reached $1 billion in revenues a decade later in 2009 and $5 billion by 2015.

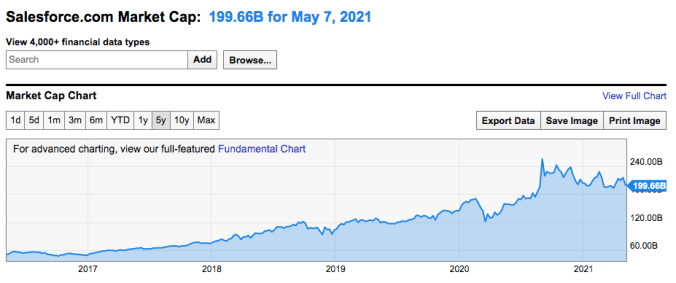

The company’s valuation grew in tandem, to $200 billion now:

To the left, you see Salesforce’s actual revenue growth; to the right, you have Snowflake’s revenue forecasts by one analyst who as of today holds the stock (so take with a grain of salt).

Investing or Trading?

If – and this is the $250 billion question – Snowflake could reach $5 billion in revenues in the mid/late 2020s, then you have a compelling case to remain bullish:

a) once the company has a few quarters of reported earnings under its belt

b) if you have a long time horizon

c) if you believe that high-flying tech stocks will continue to command high multiples relative to historical trends. If conversely you think that there’s a high risk of compression of multiples, then even if the revenues continue to grow, the company will need to grow into its current valuation (meaning even if revenue growth mirrors Salesforce’s, the market cap will be far lower than Salesforce’s valuation growth).

It’s also worth noting that since January, IBM (which really isn’t the best comparable other than their valuations converging one cold January day) has seen its market cap grow to $140 billion while Snowflake’s come down to earth at $60 billion (another sign that the market does correct itself and isn’t as exuberant across the board as during the dot com days).

For more on the competitive landscape facing Snowflake, check out my first article. My guess is Snowflake will continue to experience near term volatility and only once it shows consistent growth rates after a few more quarters, will it start to trend upwards for good. After all, the stock is expensive. If you have a short term horizon, stay away. But if you are looking for leaders in growing sectors with a long term horizon, Snowflake is worth a look at the right price.

Disclaimer: Nothing here should be misconstrued as investing advice. I am NOT licensed to give any advice. These writings are intended as entertainment to put into context how a media entrepreneur and investor thinks, given my unique time horizon and risk profile. Educate yourself, read up on mistakes others have made and speak to a licensed professional who can help you based on your investment profile and time horizon. The majority of my holdings are in safer, value stocks and managed by professionals. These investments represent riskier investments that make sense for my time horizon.

1 Pingback