Yesterday, I referenced that while in college, our final group report for the hybrid Bachelor/MBA Management Of Financial Institutions course at the John Molson School of Business at Concordia University was on the Long Term Capital Management hedge fund. Lucky for you, we found a copy. Bear in mind I was 21 at the time. Enjoy.

Since the early 1980’s, the United States has experienced a tremendous Bull Run. After the 1987 correction, investors have required higher returns on their capital. Simultaneously, many sought to diversify their investments geographically in order to capitalize on cyclical growth patterns while spreading out their risks over many regions. As new investment vehicles were being created, more and more money was being poured into the financial sector.

THE FUND THAT WAS BUILT ON SAND…

- Managers / partners

Following Salomon Brothers’ Treasury bond scandal in 1991, then vice chairman and proprietary trader (manager responsible for trading a firm’s own cash account) John Meriwether left. Gradually, a number of his former coworkers followed him to resurface in 1993. Meriwether’s brainchild was a hedge fund called Long Term Capital Management. Meriwether’s reputation as a great trader allowed him to recruit, among others, Nobel laureates Robert H. Merton and Myron S. Scholes, as well as David Mullins, vice chairman of the Federal Reserve Board until 1994. This fund was to take positions that Meriwether and partners dictated. Meriwether started Long Term Capital, which consisted of many investment vehicles: some partnerships, some corporations, some domiciled in the US while others are domiciled in the Cayman Islands for income tax reasons. All these funds pour their money into a master fund called Long-Term Capital Portfolio L.P., a Cayman partnership. Nonetheless, the fund has always been referred to as Long-Term Capital Management, or LTCM.

- Outside Investors

LTCM was distinctive from the beginning. It carried out positions that took 6 to 24 months before delivering profits. As a result, the fund ruled that investors in the fund would not be allowed to withdraw their capital quarterly or annually, which was the norm amongst hedge funds. Rather, it would force investors to lock up their minimum $10 million initial investment until the end of 1997. This effectively ensured that the potential withdrawal would be 12% of the fund’s capital. LTCM’s investors paid unusually steep fees: 2% of capital invested in the firm as well as 25% of profits.

- Returns

| LTCM’s Annualized Return on Capital | |

| YEAR | RETURN |

| 1994* | 20% |

| 1995 | 43% |

| 1996 | 41% |

| 1997 | 17% |

| * last 10 months of 1994 | |

| Source: Fortune |

- Disclosure

The hedge fund was very secretive, disclosing very little to outside investors. The lack of transparency and lengthy capital lock-up should have given investors an idea of the fund’s risk-profile. Nonetheless, investors looked the other way after the fund returned 48.3% in its first 31 months of trading with little volatility.

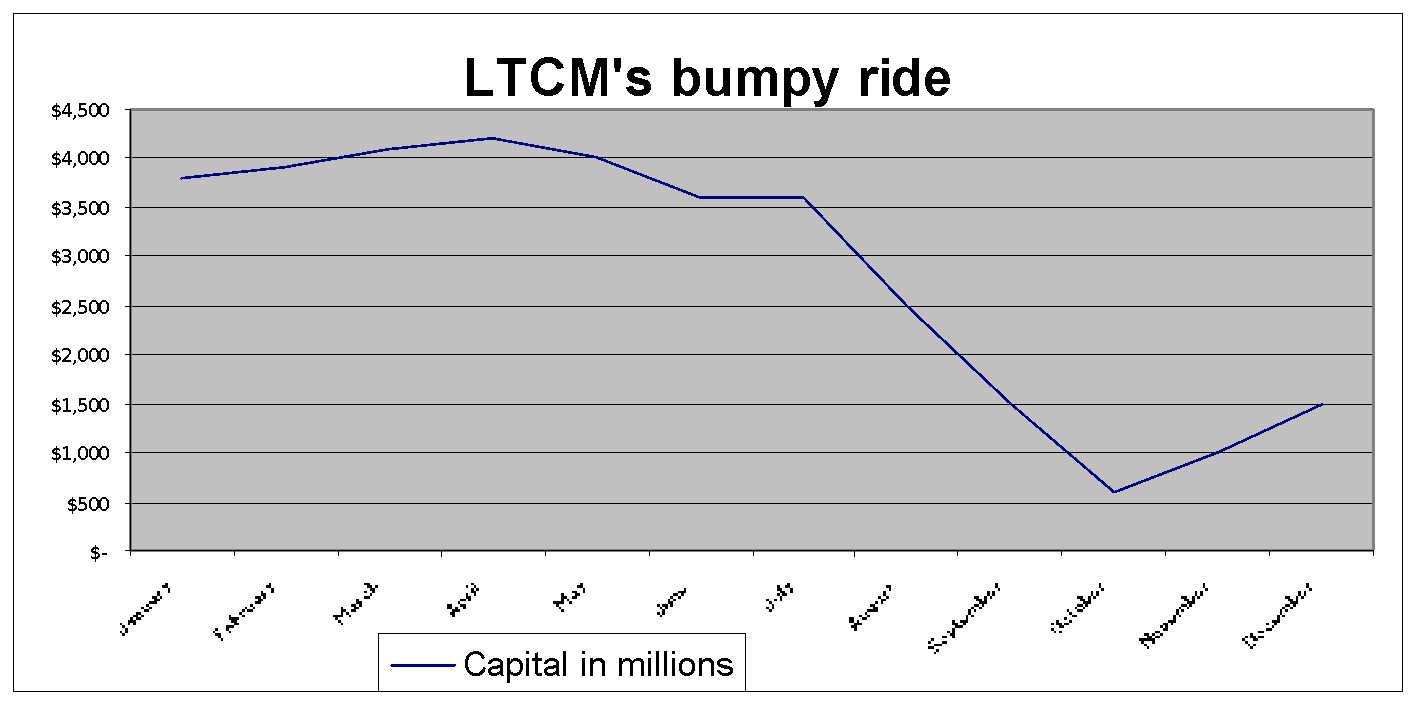

By 1997, contributions and reinvested earnings had raised LTCM’s capital to around $7 billion, at which time the managers’ greed began to outweigh their sense of logic. LTCM’s managers concluded that the fund had too much capital given its investment opportunities, forcing many newer investors to withdraw their money. By year-end 1997, the fund had $4.7 billion in capital, of which $1.5 billion belonged to insiders.

THE FUND THAT WAS TOO SMART TO FAIL…

LEVERAGE

Meriwether had acquired a near-cult following among coworkers thanks to his successful bond trading track record. Banks and brokerage firms were thrilled at the prospect of lending him money under favorable terms (by waiving collateral for example). His legendary status at Salomon and LTCM enabled him to raise capital at low cost and with few guarantees.

By 1997, the fund had about $125 billion in debt, its balance-sheet leverage ratio was 25 to one. This understated the fund’s true credit risk because it had aggressively entered into off-balance sheet derivatives contracts that, by their nature create additional leverage.

INVESTMENT STRATEGY

- Equity

LTCM’s entered the equities market in 1995 under partner Lawrence Hilibrand’s supervision, who made his name as a quantitative expert on mortgage-backed securities as head of Salomon Brothers Inc’s bond-arbitrage group. Lawrence Hilibrand was one of the two men who were in contact with Buffett during the Goldman Sachs / Berkshire Hathaway negotiations. Meriwether selected Hilibrand because of Buffett’s high regards for him.

By June of 1998, the fund owned $539.2 million worth of stocks in 76 companies. The fund felt that its bond expertise was transferable to stocks. Conceptually, their equity arbitrage strategy was similar to what the firm was doing with bonds: long on the cheap security while short on the expensive one, based on historical trends. The firm’s equity trading strategy fell under three main categories:

a) Pairs trading (two related stocks: parent/subsidiary or two firms in similar industry)

LTCM had a $2.3 billion position in Royal Dutch Petroleum and Shell Transport. Historically, Shell had sold at an 18% discount to Royal Dutch. When the discount rose above that, LTCM bet that Shell was cheap compared to Royal Dutch. So, LTCM bought shares of Shell Transport while selling shares of Royal Dutch. If oil stocks go up, Shell would rise more than Royal Dutch would. If oil stocks go down, Shell would fall by less than Royal Dutch. Unfortunately for LTCM, the stocks diverged even further.

b) Risk Arbitrage

Rather than going long on one stock and shorting the other, LTCM entered into total return swaps with Wall Street firms. This allowed LTCM to pump up returns through leverage and shift most of the risk to its trading partners on Wall Street. Take for example Citicorp and Travelers Group. Based on the terms of the merger, Citicorp was relatively underpriced. Instead of buying Citicorp, LTCM bought a total return swap from a bank, whereby the bank would pay LTCM the total return on Citicorp stock (stock appreciation and dividend). If, on the other hand, Citicorp declines, LTCM must pay the banks the decline in the stock price. The advantage of such a strategy is high stakes gambling without a penny in margin. The disadvantage to risk arbitrage is that if the fund is wrong, they must pay up afterwards.

c) Market Volatility

LTCM bet that the wide swings in the markets would revert back to historical norms. The more volatile a stock, the more expensive are the puts and calls. Similarly, the more volatile a market, the more expensive are the prices of puts and calls on the index. LTCM felt that volatility was abnormally high. LTCM was short volatility, but it increased sharply, forcing LTCM to put up more collateral to cover losses and maintain its options positions.

- Fixed-Income Securities

a) Arbitrage

Very few of LTCM’s bets carried direction or position risk. Instead of betting on which way the market was headed, LTCM would search for arbitrage plays: opportunities to profit from temporary disparities in prices of related assets

By putting its financial technology and experience to work at finding sectors of the bond market in which yields had gotten out of line with yields in related sectors, LTCM captured small profits from carefully hedged positions by buying the cheap security and shorting the expensive one.

Much of LTCM rationale was based on historical performance: converging spreads between risky and risk-free assets. Under such scenario, the fund does not care whether rates go up or down, as long as they converge.

b) Market integration in Europe

Their reasoning was also intuitive. As Europe sought to integrate markets, it had to ensure that the 11 member countries would align their interest rates. Italy’s Central Bank, for example, would have to reduce inflation and lower its rates through monetary and fiscal policy in order to align them with the lower German rates. If not, different rates would present huge arbitrage opportunities once the Euro currency would begin trading.

c) Quantitatively oriented

LTCM is one of the 20% of hedge funds that are quantitatively oriented. By inputting financial data into computer models, LTCM could pinpoint profitable strategies while simultaneously “spitting out” the hedging strategy to limit risk.

Confident that its position risk was very low, the fund proceeded to take on colossal balance-sheet risk, seduced by the most addictive drug in finance: leverage. The fund’s annualized return per dollar was 67 basis points (0.67¢). Leveraged 30 to one, a 0.67% return on each dollar at risk would mushroom to 20% per annum, with little apparent risk. The beauty of “rocket science” in finance was that while the gambles were huge, the risks seemed minimal.

d) Computer Models

LTCM’s Achilles heel was that it believed that its computer models were full proof. Such bets failed because various factors were not fully incorporated into the models:

- Lack of liquidity: When a computer program pinpoints a profitable hedge, the assumption is that there will be a buyer on the other side of the transaction when the deal is settled. But the turmoil in Russia and Asia so unsettled markets that buyers disappeared.

- Breakdown of international diversification patterns: Usually traders can hedge their bets by investing in many different geographical regions. But the patterns changed, whereby a decline in one region was not being offset by a rise in another.

- Limited application: models that may be useful for countries with well-developed markets do not necessarily work well in smaller, less-developed markets.

- Missing street smart: many mathematical geniuses with little practical experience in financial markets have been hired by Wall Street. Black box models put on autopilot, without review or input by seasoned traders, can fail.

- Political risk: the models failed to realistically assess the risk that Russia would backslide so abruptly on the road to capitalism.

In order to function properly, computer models require liquid markets with demand on both sides of a transaction. But markets are thin in August as Meriwether himself told fundholders that “volatility and [the] flight to capital were magnified by the time of year when markets were seasonally thin.” What exasperated such a shock was the worldwide phenomenon of liquidity drying up across markets. As a result, the geographical diversification strategy employed by most firms did them no good.

One critique of such complex models is the assumptions they make about market volatility. The Black-Scholes options pricing model is highly regarded, but it tends to underestimate how volatile markets tend to be in times of irrationality, be it on the upside or on the downside. While models estimate about four times volatility in periods of turmoil, historical data would suggest that volatility could hit up to 12 times regular price swings.

Finally, model risk is an equally important factor to consider for quantitative-oriented firms. There exists the risk that the model in question may be different than what actually occurs in markets, especially with such data-in, data-out models.

In a sense, the problem was not too much rocket science but not enough. The problem with the models was that they did not assign a high enough chance of occurrence to the scenario in which many things go wrong at the same time – the perfect financial storm. Apparently, the worst-case scenario envisioned by LTCM was about 60% of the one that actually occurred. LTCM believed that its financial technologies and meticulously constructed hedges gave the fund a conservative risk profile, as spelled out in October 1994 in a proposition to investors. The paper contained a range of returns that the fund could aim for with the respective probability of loss if things went bad. For example, the table said that if the fund would be shooting for a 25% return, the probability that it would end up losing 20% or more was an insignificant 1 in 100. The table never even contemplated a steeper loss.

THE PERFECT STORM AND ITS RIPPLE EFFECTS

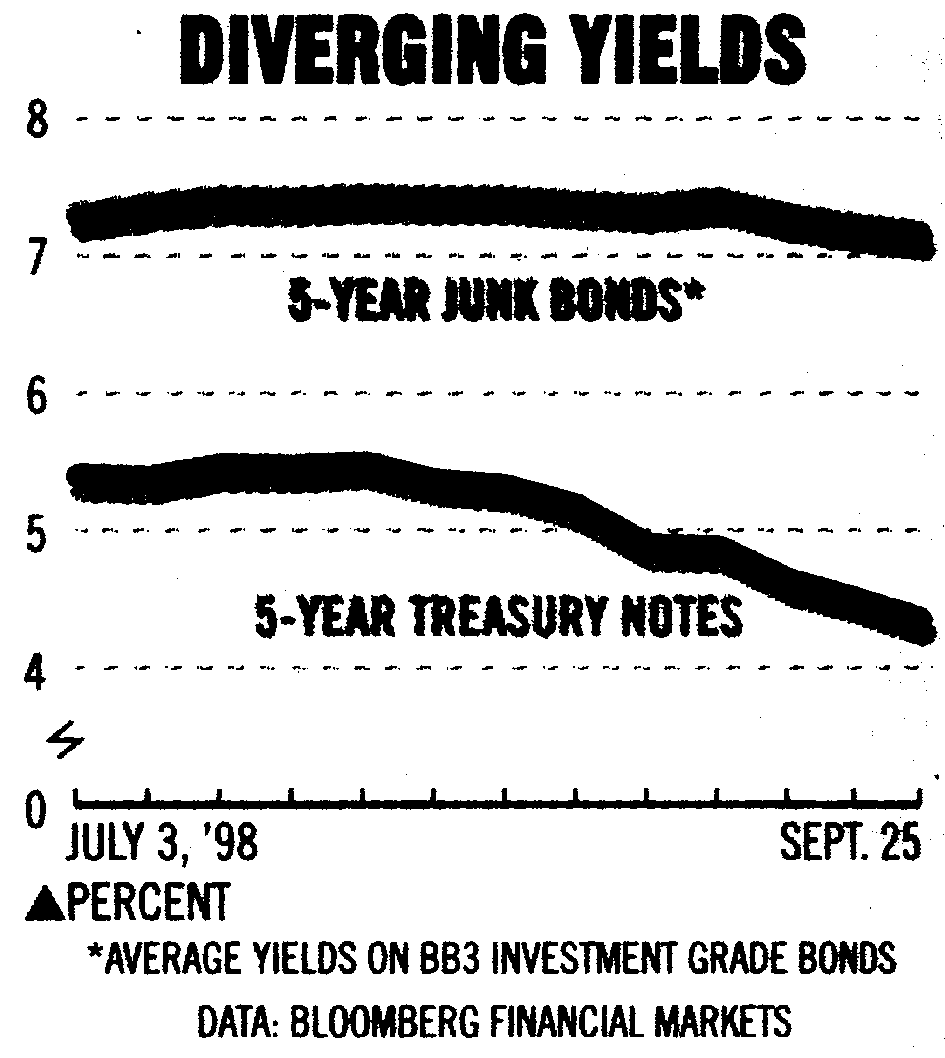

What occurred in August of 1998 was the financial world’s equivalent of a perfect storm: everything going wrong at the same time. Interest rates moved the wrong way, stock and bond prices that were supposed to converge diverged, and liquidity dried up in many markets.

Even though LTCM had little direct exposure to Russia, July’s debt default on short-term liabilities drastically reduced investors’ appetite for risk. The signal to international investors was clear. Quickly realizing that an emerging market label means little when the economy rests on weak fundamentals: lack of accountability, failure to collect taxes and pay employees, and excessive corruption. Moreover, “earning” 100% returns are insignificant if the borrower has no intention or is incapable of repaying back the loan.

- Flight to Quality

What followed was a massive flight to quality as investors switched their investments into the safest haven they could find: the US market and the US dollar. As investors sold foreign, riskier securities, their prices fell while rates rose. Conversely, US securities’ prices rose and rates fell. Most of the quantitative firms were betting on riskier, less liquid securities such as corporate and junk bonds.

Instead of narrowing, the spreads between risky and risk-less securities widened in virtually every market around the world, crushing Meriwether’s fund.

- Capital Inadequacy

Those who bled most were the highly levered firms, such as LTCM. When spreads widened in a disorganized tumbling market, gains on short positions were not enough to offset gains on long ones. Lenders demanded more collateral, forcing funds to either abandon the arbitrage plays or to raise money to meet margin calls by selling securities at fire-sale discounts. By September 2nd 1998, LTCM’s capital had fallen by 44%, to $2.3 billion, while still carrying over $100 billion in debt.

- Liquidity Problem

Although LTCM did not have an internal liquidity crisis (fundholders could not after all withdraw their capital), it did suffer from one, especially after forcing many investors to withdraw their funds earlier given a lack of investment opportunities.

- Credit Crunch

The repercussions of a LTCM bankruptcy would have been far greater than anyone could have anticipated. LTCM’s investors were the managers of the fund, wealthy individual investors, big banks and large brokerage firms. Drawing the line between creditor and investor is hard: some of the banks that were lending Meriwether money under favorable terms had also invested in the fund. Considering that much of the fund’s funds came from banks, a bankrupt LTCM would have forced many banks to declare huge losses on their gambles (many had after all unsecured loans with the firm). The potential for huge losses for so many different banks was too much to contemplate, leading to a credit crunch of huge dimensions. Others who eventually bailed the fund out maintain never having invested a penny in the fund, such as Deutche Bank. Nonetheless, the fund’s welfare was to have far greater repercussions than any other fund’s returns would.

Europe’s UBS was one bank which both lent and invested in the firm. The bank’s senior managers had so much faith in the gurus from Greenwich that it put up more than $1 billion at risk in LTCM, without even protecting itself against a decline in the value of LTCM. It violated the first rule of risk management: downside protection. When the mess was over at UBS, it cost them about $700 million and four top executives, including Chairman Mathis Cabiallavetta.

LTCM’s near death experience was the first internal shock to the US financial system. Although Asia, Russia, and now Latin America pose serious threats to the American economy, LTCM’s collapse would have been the uppercut to a shaky environment in the wake of Russia’s debt default.

SOLUTIONS

- Federal Reserve Board and Alan Greenspan

For most of September 1998, LTCM hung on the edge of bankruptcy. The Federal Reserve was trying to avert the domino effects that a fast liquidation of the fund’s holdings would have on an already reeling global securities market. The Federal Reserve Chairman, Alan Greenspan appointed the Fed President William McDonough, who coordinated the process. He oversaw the negotiations and brought the creditors together. Every bank had sent its CEO or another top executive. While none of the participants really wanted to ante up the money, all dreaded a bankruptcy.

- Berkshire Hathaway, American Insurance Group, & Goldman Sachs

Once the negotiations got underway, a curve ball was thrown to the Fed by Goldman Sachs, one of the many investors / creditors of the fund. Goldman Sachs was to join forces with Warren Buffett’s Berkshire Hathaway in a bid for the fund. Berkshire Hathaway would put up $3 billion, $700 million would come from AIG (whose head Hank Greenberg is a close ally of Buffett), and $300 million would come from Goldman Sachs. The bid was sent to Meriwether, who initially refused the deal because he said he could not get the other partners’ approval in time. He then argued that it was structurally flawed, whatever that meant.

Buffett has his own interpretation. His deal would have left LTCM’s managers with little money and no jobs. LTCM’s fate was uncertain because of the then abnormal market conditions. However, most participants had strong beliefs that the fund would eventually return to profitability. Meriwether’s problem was that he lacked the funds to meet margin calls. A large bank or Berkshire Hathaway (which at the time was sitting on $10 billion) has more than enough capital to weather the storm. The Buffett proposition went back and forth, but died eventually because Meriwether did not want to give up control of the hedge fund he started. Meriwether had a lot of clout in the decision-making process. He could have let LTCM go bankrupt, instead of giving up control.

Interestingly, Buffett’s investment strategy has always emphasized simplicity. He avoids technology stocks for this reason, and the same rationale would make one wonder why he would be interested in investing in such a high risk (highly levered), arbitrage-seeking investment vehicle. Firstly, Buffett had already saved Meriwether and Salomon after the Treasury bond scandal.

At the time, Salomon admitted to violating Treasure auction rules when it was controlling 95% of the two-year Treasury-notes. Treasury rules state that firms cannot auction for more than 35% of the total offering. In the chain of disclosure, senior Salomon official Paul Mozer admitted to Meriwether in April 1991 that he had falsified bids for Treasury securities. Meriwether went to his bosses, everybody concluded that the Fed had to be informed, but no one did the telling. When the scandal erupted in August, Mozer was fired. Meriwether’s bosses (John Gutfreund and Thomas Strauss) resigned under pressure. To the rescue came Buffett, head of Salomon’s biggest shareholder, Berkshire Hathaway. Initially, Meriwether’s fate was still uncertain. Because Buffett believed that Meriwether had acted responsibly by telling his bosses, Buffett was not sure wether it was fair to fire Meriwether. In the end, Meriwether himself resigned, saying it was best for the firm.

Also, Buffett’s empire would surely have suffered had LTCM gone bankrupt, pushing several large banks into bankruptcy. Although Buffett’s bid was made because he knew that the fund would earn attractive returns with time, it can be argued that his decision to pursue the fund was also made to avoid the catastrophe that would have followed LTCM’s bankruptcy.

- Consortium of 14 banks

Although Buffett’s bid made a lot of sense, it eventually died as Meriwether showed little interest. The Fed then had to orchestrate another alternative. When the dust settled, the hedge fund was rescued by a consortium of 14 banks and brokerage firms with a $3.6 billion infusion to restore capital adequacy in exchange for 90% of the fund, allowing Meriwether and friends to retain 10% of the fund. Each bank eventually invested $100 to $350 million.

By November, the consortium had begun to turn things around, albeit by a mere 1% increase in portfolio value. The fund’s net asset value has climbed about 14% from the end of September to the end of December. The portfolio has netted the banks and managers a healthy 10%. Although such returns would have called for a $50 million year-end bonus for Meriwether and friends (15% cut of all profits above LIBOR, as well as a 1% management fee on the $4 invested), it turns out that the original managers will simply receive their base salaries of $250,000. The bonus money will cover the legal expenses of the bailout.

LONG TERM LESSONS…

Although private and institutional investors have lost fortunes on the markets with little or no compensation, the Fed did, in hindsight give preferential treatment on fears that the bankruptcy of a fund that owed upwards of $100 billion to banks would wreak havoc like never before seen. That second 25 basis point rate cut was done to further insulate the US economy from the international financial storm, but it was also done to keep banks from doing what they are suppose to do: lend and invest to stimulate growth. By keeping their cost of capital down, the Fed was ensuring that any potential losses from LTCM would not force banks to stop lending.

It is ironic nonetheless that the US Treasury department moved at such rapid speed to save a private boys club, even though it has taken extremely long to restructure troubled economies abroad where the lives of millions are at stake.

Most are urging the government to restrict leverage. While most typical hedge funds beef up their equity positions by 30%, LTCM’s leverage ratio was an atypical 25 to one ratio. Nonetheless, excessive leverage is often required for such technical bets to be profitable. Regardless, LTCM’s near-disaster proves that the risks from overblown leverage do not justify the rewards they can provide a few superrich traders and their bankers. Interestingly, Asia succumbed to crony capitalism and loose lending. The latter is also what rocked LTCM. While Japanese banks were lending capital against inflated assets, LTCM was borrowing thanks to its reputation and historical performance.

Another point is the lack of disclosure to shareholders. No one cried foul when LTCM disclosed little while returning above 40% to fundholders. Once things went bad, then investors and regulators began to expose the virtues of increased disclosure. Excessive restrictions on leverage, or urging further disclosure could force more hedge funds (and businesses in general) to relocate to environments were they are allowed to operate as they wish.

Many hedge funds weathered the storm because they had hedged themselves, they had not speculated by taking on too much balance sheet risk. Initially, many called this high-IQ hedge fund from Greenwich the hedge fund that was too smart to fail. Following their near-death experience, it turned out that LTCM was too smart to fail. It had, perhaps inadvertently, shifted most of the risks to their banker friends.

ENDNOTES & EXPLANATIONS:

Business Week, September 21st, 1998, “Failed Wizards of Walled Street,” Coy, P., Woolley, S., Spiro, L.N., Glasgall, W.

Fortune, October 26th, 1998, Loomis, C.J., “A House Built on Sand,”

Managed Money Review, “LTCM: Should Investors have known?” November 1998.

The Financial Post, September 24-26th, 1998, “The hedge fund that was too smart to fail.”

Business Week, November 9th, 1998, “How Long-Term Rocked Stocks, Too,”

“The Al Capone Link of LTCM,” October 4th, 1998

“Richard Olsen knows why LTCM went wrong,” October 21st, 1998,

Business Week, November 11th, 1998, Laderman, J.M., “UBS Failed Risk Management 101,”

Business Week, October 12th, 1998, Spiro, L.N., “The Rescue: What you Need to Know,”

“LTCM back in black,” November 11, 1998.

The National Post, Wednesday, February 3, 1999, Reuters, “Two partners retire from hedge fund,”

August, O., “No Bonuses but a Nice Salary for Leaders of Botched Hedge Fund,” December 30th, 1998

4 Pingbacks